New Congress Bill Fights Visa and Mastercard’s Duopoly

In September, retailers signed their support of the Credit Card Competition Act faster than my wife can click “buy now” 200 times on Prime Days.

My bank account may recover, but Visa and Mastercard are sweating more than the delivery driver unloading those 200 boxes.

In July, Senator Dick Durbin and Senator Roger Marshall introduced the bipartisan Credit Card Competition Act of 2022. In September, Congressmen Peter Welch and Lance Gooden introduced the House companion.

Over 1,600 companies and 200 trade associations sent supporting letters to all the members of the House and Senate. The message is clear:

“THESE FEES ARE TOO $%^& HIGH!”

Here are a few of the critical issues that are more infuriating than printing 199 return labels to take back all the Prime Deal regrets (sometimes you have to learn the hard way):

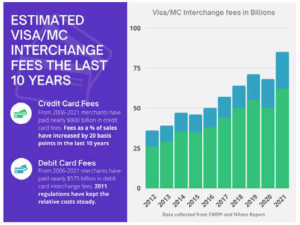

- Visa & Mastercard account for 83% of all cards issued in the S., and they set the swipe fees charged by the banks (these fees make up 70-90% of total processing fees). Visa & Mastercard do not let the issuing banks use alternative payment networks.

- They “update” fees twice a year in April and Swipe fees have doubled in the last decade, increasing more than 25% last year alone.

- This year, the average American household will see nearly $900 in fee-related inflation to their goods.

- U.S. Processing Fees are nearly 7x more than E.U. Processing Fees.

- In 2021, S. Merchants paid more than $138 billion in processing fees.

THE GOALS OF THE BILL ARE SIMPLE:

- Increase Competition & Lower Fees: Force Visa and MasterCard to allow alternative networks (e.g., NYCE, STAR, ) to process their transactions. Merchants currently have no leverage with Visa and Mastercard. Alternative networks would allow merchants the ability to choose and negotiate fees. Estimated merchant savings could reach $11 billion by introducing more competition.

- Increase Security, Reliability, and Redundancy. Merchants are left in the dark when Visa or Mastercard have network outages. With the ability to process on alternative networks, these outages would have minimal impact. Additionally, more competition would drive innovation in security, reducing fraud and penalty fees.

WHEN WILL I SEE THE BENEFIT OF THIS LEGISLATION?

If it’s passed and If (BIG IF) you are on a “Pass-Thru pricing” model, you could see these changes begin next year.

If you are on a “blended rate” or “tiered pricing” model (Major Fuel Brands), you have a second battle to fight! Your processor will benefit from these changes, but you must negotiate with them to pass along the lower fees!

If you want to know more about how your processor is involved or if you aren’t sure what pricing model you have, let us know today! We’d be happy to help clear it up for you.

Did you join in with thousands of retailers voicing their support? If so, we’d love to hear from you!

KC Cook

Founder & President

KC COOK | PIX

p: 919.215.7908

e: kc@trypix.io

w: pixcardprocessing.com